For decades, the idea of owning a home has been a key part of the American dream. A white picket fence, two kids, and a golden retriever with a manicured lawn, and friendly neighbors. Homeownership is a symbol of financial stability and success, as well as a great long-term investment.

However, in the decade following the Great Recession and the housing market crash of 2008, many people struggled to afford a home. Mortgage lenders are much more regulated with stricter criteria for people to meet before they pre-qualify for a home. Long gone are the days of a mortgage promised with zero down payments and a low credit score!

One major change in the market has been the growing trend of rent to own homes. Many people are finding it easy to get into a rent to own home near them and are living their homeowner dreams. Click here to see if you qualify (it’s simple and quick).

Can You Get a Rent to Own Home With No Money Down?

While having stricter criteria for mortgage lending practices is an overall improvement, it has made it much more difficult for low-income people to achieve the aforementioned key part of the American dream. They are continuing to throw money away on rent every month to delay the inevitable rejection from a mortgage lender.

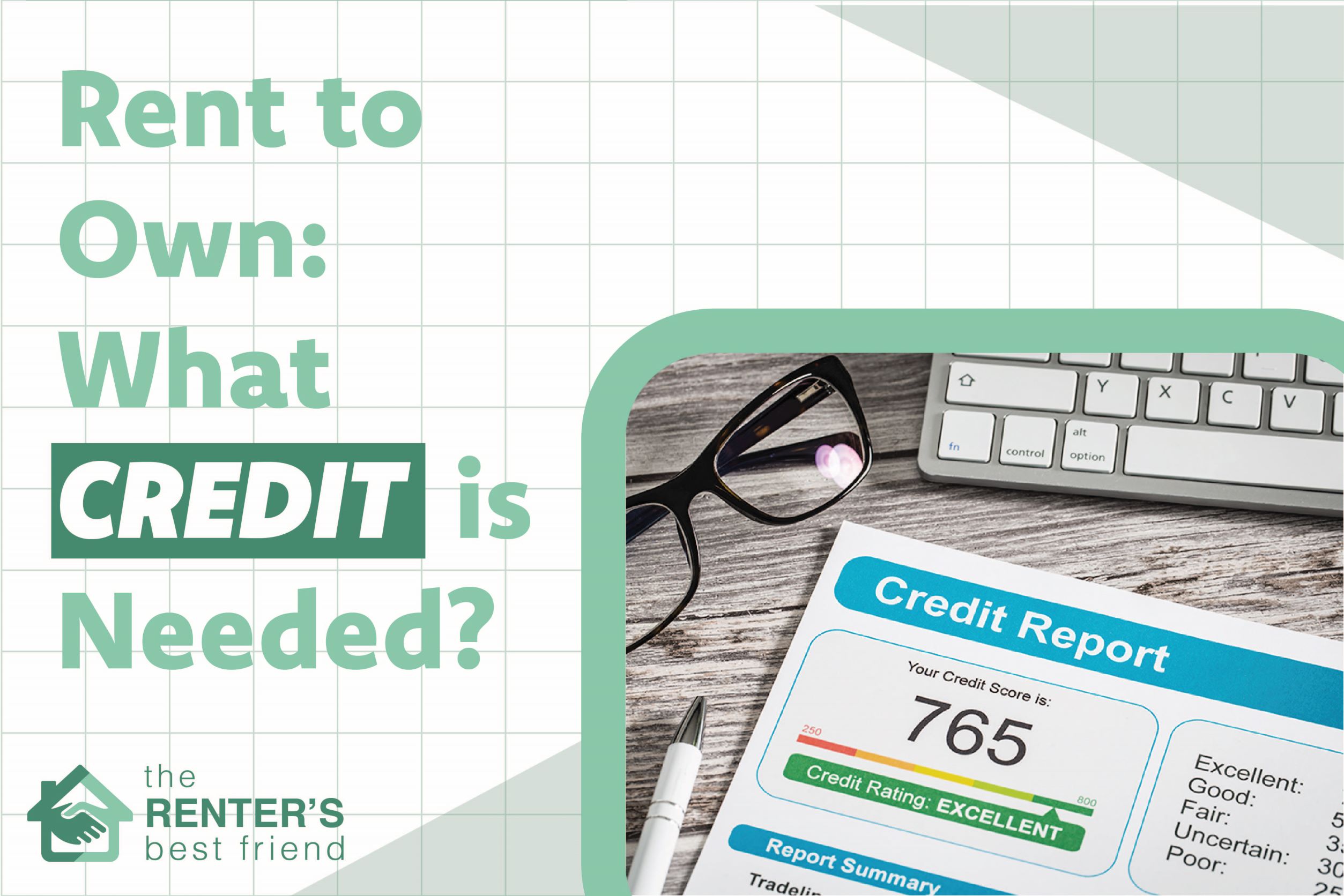

These rejections could be because they don’t have enough money saved for a down payment or they have a poor credit score. Maybe they have switched jobs a few too many times and they don’t have the stability of employment longevity that most lenders look for. It’s either outright rejection or the interest rate is insultingly high.

Something that many people don’t realize is that they can qualify for housing assistance (or help getting a home). Don’t miss out– take advantage of the help. Click here to check into the housing benefits available near you.

If you find yourself looking to build your credit while also investing in the future purchase of a house without the costly upfront costs, you may consider looking into a rent-to-own home.

A rent-to-own home agreement works like a traditional lease, except with a special caveat: you agree to buy the house at the end of the lease for a specified purchase price. You will pay rent on the property, with a certain portion of the rent to be put aside in an escrow account for the down payment.

When you enter a rent-to-own agreement with a seller, you will both agree to:

- The rental fee and the rental credit which will go toward the future purchase price of the house.

- The length of the lease agreement. These agreements are typically 1 to 5 years.

- The purchase price is based on the market value at the time of signing the lease.

There are some upfront costs that you will need to consider when signing a rent-to-own agreement. Like most rental agreements, you will likely need to put down a security deposit. A lot of the time the seller will require a larger, non-refundable deposit than what you would expect to pay when renting an apartment or house; sometimes this can be up to 10% of the total purchase price of the house. However, most sellers will work with you to lower the payment, like setting up a payment plan with your rent over the first few months.

You will also pay an option fee, which is based on a certain percentage of the future purchase price of the house. While down payments in a traditional mortgage are usually 20% of the total purchase of the house, option fees range from 2 to 7%, depending on the agreement that you make with the seller. There is no standard rate, so definitely negotiate with the seller to get a lower rate in exchange for a higher monthly rent payment.

While mortgage lenders no longer advertise homes for zero down payments and you will be hard-pressed to find any financing options without any money upfront, rent-to-own homes are a great way for you to build your credit rating and save for the future purchase of the house.

You will have some upfront costs – most of which are negotiable with the seller – and you will have to agree to all the lease terms set by the seller, but you will have time and the flexibility that does not come with a traditional mortgage.

Again, don’t miss out on your rent to own home possibilities– see if you qualify by clicking here.